As fascinated eyes turn to admire the burgeoning offshore industry, analysts and wind farm entrepreneurs underline the intensifying demand for vessels amid the sector’s growth. A recent in-depth market report composed by Intelatus Global Partners amplifies this concern, focusing primarily on the challenges faced by the floating offshore wind energy segment.

The Dire Need for Vessels in Offshore Wind Farms

A predicament proliferating within the industry is the insufficiency of apt vessels, a concern by top-tier developers who underscore this as a potential roadblock to their plans. According to Intelatus’ findings, capital expenditure for this division alone will surpass a remarkable $250 billion by 2035. However, this promising surge could potentially be deterred by the scarcity of vessels equipped to fulfill the needs of the sector.

The Spectacular Growth in Floating Wind Capacity

The global floating wind capacity is estimated to witness a dramatic rise, projected to climb from 200 megawatts at the end of 2022 to approximately 61 gigawatts in the next twelve years. To attain this figure, the report approximates the necessity to pre-lay beyond 6,000 mooring spreads, with the anticipation of hooking up around 5,400 turbines.

The Upsurge of Business Opportunities in Vessel Ownership

For vessel owners, the spectrum of market opportunities, varying from straightforward transport and assembly to comprehensive floater engineering, procurement, and constructions, will total anywhere from $28 to $145 billion, as per Intelatus. The study pinpoints two categories, namely, anchor-handling vessels and subsea construction vessels as those that will experience the highest demand in support of the burgeoning floating offshore wind expansion. They project nearly $12 billion in shipbuilding activity in the short to medium term to support the advancement of floating wind farms.

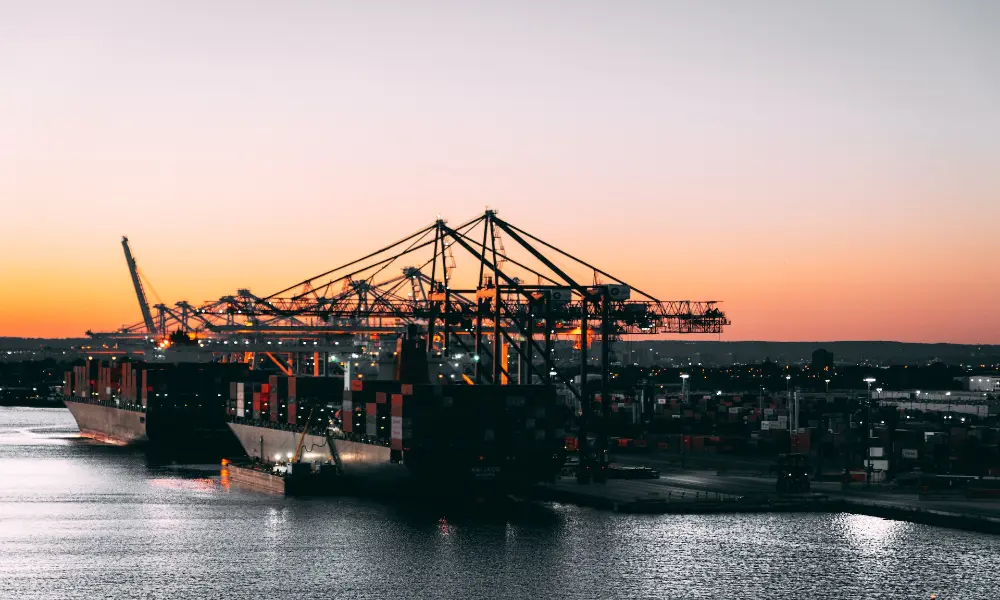

The Pivotal Role of Anchor Handlers

The primary vessel type deployed to pre-lay, tow, and hook up a majority of floating wind turbines are anchor handlers. Despite a global fleet of approximately 2,400 anchor handlers, Intelatus conveys that a scant 50 are identified as suitable and effective for floating wind projects. Intelatus reveals that the dearth of shipbuilding capacity and extended lead times for new vessels will indeed become pertinent issues for the increasing wind sector.

The Reignited Oil and Gas Activities: A Double-Edged Sword

A further challenge inhibiting success in the floating wind sector is the revival of oil and gas activities. This resurgence, causing a hike in competition for accessible capacity, is decreasing the availability of suitable vessels to undertake floating wind project installations.

The Imminent Challenge of Installation Capacity

Top wind farm developers are not oblivious to the impending issue of limited installation capacity. Ōrsted, a pioneering worldwide developer of offshore wind farms, recently recounted an array of problems hampering its U.S. projects, which it predicts may lead to an impairment charge escalating to a staggering $2.3 billion. Amidst these problems is the glaring shortage of installation vessels, which Ōrsted foresees causing significant delays and escalating costs. The bleak outcome has led Ōrsted to consider abandoning several U.S. projects, attributed to the altering financial dynamics and the anticipation that the financial return criteria for development will no longer be met.